- News

- Business News

- Do you need a high value health cover?

Trending

This story is from September 7, 2015

Do you need a high value health cover?

A significant rise in medical inflation has seen health insurance companies offering very high value covers.

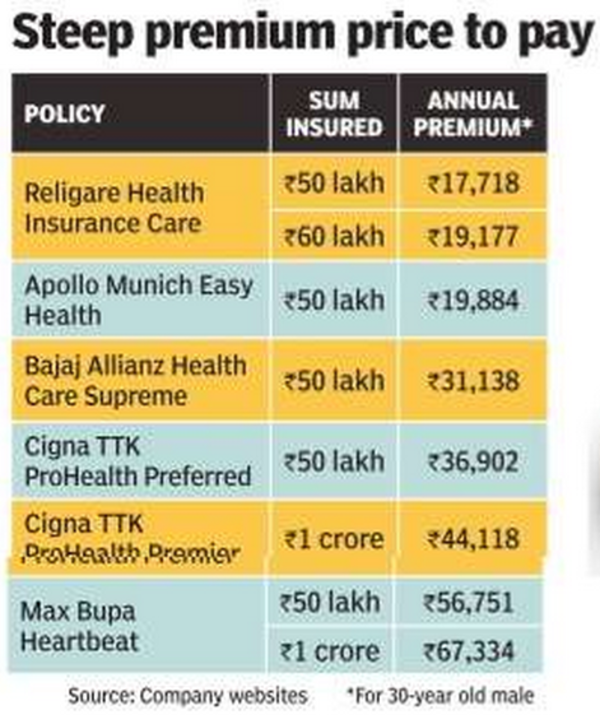

A health insurance floater policy of Rs 5 lakh was considered adequate till recently. However, rising healthcare costs are pushing individuals to opt for higher covers. Cashing in on the trend, some companies are now offering Rs 50 lakh, and even Rs 1 crore covers. Apart from hospitalization costs, these high-value policies offer higher maternity, baby care, post-treatment, OPD and day-care procedure covers, insure organ donation and fund alternative treatment.

Not surprisingly, the premiums are steep. An individual health cover of Rs 50 lakh for a 30-year-old would cost Rs 20,000-60,000 a year. A family floater of a similar sum insured would cost Rs 40,000-50,000 if the oldest family member is 30-35 years old. How much do you need?

Divya Gandhi, Principal Officer and Head of General Insurance, Emkay Insurance Brokers, says a Rs 20-25 lakh policy is sufficient even if you plan to get treated in the best of hospitals in metros. "The entire sum assured doesn't get utilized and the high premium is wasted as not many claim for more than Rs 20 lakh a year," she says. The biggest advantage of high value covers is that international treatment is compensated. However, the list of ailments covered is restrictive. Usually treatment abroad is covered for diseases like cancer, benign brain tumour, major organbone marrow transplant, heart valve replacement and coronary artery bypass graft. An overseas treatment claim is honoured only if similar treatment is not available in India.

These policies also have a higher co-payment clause for senior citizens at 20%. According to certified financial planner Abhinav Gulechha, the year-on-year premium cost does not justify the coverage provided. What are your options?

Assuming you may still consider going overseas for a specialized treatment, you could buy a fixed benefit policy like for critical illness, in combination with the regular hospitalization cover. You could also buy a high-sum insured critical illness plan and get the entire sum insured as lump sum. High-value covers are beneficial if you are looking to cover your family.

They do not apply sub-limits on room rent. Some policies also cover treatment abroad and allow reinstatement of sum insured.

Not surprisingly, the premiums are steep. An individual health cover of Rs 50 lakh for a 30-year-old would cost Rs 20,000-60,000 a year. A family floater of a similar sum insured would cost Rs 40,000-50,000 if the oldest family member is 30-35 years old. How much do you need?

Divya Gandhi, Principal Officer and Head of General Insurance, Emkay Insurance Brokers, says a Rs 20-25 lakh policy is sufficient even if you plan to get treated in the best of hospitals in metros. "The entire sum assured doesn't get utilized and the high premium is wasted as not many claim for more than Rs 20 lakh a year," she says. The biggest advantage of high value covers is that international treatment is compensated. However, the list of ailments covered is restrictive. Usually treatment abroad is covered for diseases like cancer, benign brain tumour, major organbone marrow transplant, heart valve replacement and coronary artery bypass graft. An overseas treatment claim is honoured only if similar treatment is not available in India.

These policies also have a higher co-payment clause for senior citizens at 20%. According to certified financial planner Abhinav Gulechha, the year-on-year premium cost does not justify the coverage provided. What are your options?

Gulechha suggests buying an indemnity plan of up to Rs 5 lakh and increasing it as and when your requirement or responsibilities increase by way of a top-up policy. Vishal Dhawan of Plan Ahead Wealth Advisors says review your health insurance portfolio every three years and then decide whether to increase it or not. You could take a call based on increase in salary, family responsibility, change in job profile and so on.

Assuming you may still consider going overseas for a specialized treatment, you could buy a fixed benefit policy like for critical illness, in combination with the regular hospitalization cover. You could also buy a high-sum insured critical illness plan and get the entire sum insured as lump sum. High-value covers are beneficial if you are looking to cover your family.

End of Article

FOLLOW US ON SOCIAL MEDIA

Hot Picks

TOP TRENDING

Trending Stories

In Business

Entire Website

- Will banks open only for 5 days a week? Here’s what you should know about IBA’s proposal

- India set to be third largest economy, says S&P Global

- Dalal Street bull run continues! BSE Sensex crosses 69,000 for the first time; Nifty above 20,800

- Byju’s reduces notice period for employees as troubles mount

- Sensex surges over 900 points, Nifty above 20,550 as BJP state election wins bolster Modi's Lok Sabha 2024 prospects

- UltraTech to buy building materials business of Kesoram in 7,600 crore deal

- Tata Technologies stock debuts at a bumper 140% premium; share price at Rs 1200 on BSE

- Tata Technologies share allotment: How to check IPO allotment status, listing date, GMP

- BSE m-cap rides rally in Adani stocks, tops $4 trillion

- Charlie Munger, who helped Warren Buffett build Berkshire, dies at 99

- Kolkata police commissioner, two health officials removed after Mamata's meeting with docs

- BAPS swaminarayan temple vandalised in New York; 'unacceptable', says Indian consulate

- Will Atishi replace Arvind Kejriwal as Delhi CM?

- 'Look at own record': India condemns remarks by Iran's Supreme Leader Khamenei

- Watch: BJP MLA falls on rly tracks while flagging off Vande Bharat train

- 'Political rivals but ... ': BJP's reaction on Bittu's Rahul 'No. 1 terrorist' remark

- Cow vigilantes killing a Brahmin is the wake-up call India needed

- Apple's biggest 'iPhone update' for year 2024 rollout starts today

- MHA to open Kendriya Police Kalyan Bhandars for civilians in Manipur

- UPS vs NPS Calculator: Switch a no-brainer? Not really! Check top points

Popular Categories

Hot on the Web

Top Trends

Prince HarryWho is Ryan RouthUPI Transaction LimitArvind Kejriwal ResignationNEET UG Admission CriteriaKolkata Doctor Rape CaseUS Presidential ElectionsRohit SharmaSports Stars Turned Power CouplesIBPS RRB Clark PO ResultDonald TrumpCristiano RonaldoIndia vs Korea HighlightsBMW Accident Madhya PradeshUPS vs NPS CalculatorMiami Dolphins OwnerLive Cricket Score

Trending Topics

Living and entertainment

Latest News

Who was Illia 'Golem' Yefimchyk, the Belarusian bodybuilder who consumed 2.5 kg of meat and 108 sushi pieces daily before his death at 36?Vempalle Shareef's story is now a lesson for degree students in Andhra PradeshGovt launches programme to tackle glacial lake outburst flood threat in Himalayas, all 190 high-risk lakes to be monitoredKhatron Ke Khiladi 14: Shalin Bhanot hosts a fun party for his co-contestants Krishna Shroff, Abhishek Kumar, KaranVeer Mehra and othersAstrological Influence on Zodiac Signs' Career ChoicesBike rally held to raise voter awareness in Jammu and Kashmir's Doda ahead of assembly electionsFalcons' Predictable Offense and Cousins' Prime-Time Woes Spell Trouble in PhiladelphiaLiza Colon becomes 1st Latina to win Best Supporting Emmy Award'Oh no!': Hilarious goof-up leads to missed catch, leaves bowler in smile. WatchJr NTR on shooting under water scene for 35 days in 'Devara Part 1': It is an important sequence!Top NFL Superstars Who Are Vegan: Derrick Morgan, David Carter, Theo Riddick and moreKSCA Invitational: Arjun Tendulkar takes match haul of 9 wickets in big Goa CA XI winAbhishek Kumar shares selfies with Alia Bhatt; recalls the time when he worked as a crowd artist in ‘Humpty Sharma Ki Dulhaniya’Jessica Gunning wins her 1st Primetime Emmy for 'Baby Reindeer'Shocking! Man celebrates birthday by lying among massive PythonsSohum Shah says 'Tumbbad 2' will be different from 'Munjya' and 'Stree 2': 'They are not making dadi-nani ki kahaniyaan'1031 candidates to contest Haryana Assembly Elections to be held on October 5: CEO J AgarwalSathiyan set to partner Sreeja in mixed doubles

Copyright © 2024 Bennett, Coleman & Co. Ltd. All rights reserved. For reprint rights: Times Syndication Service